The 401(k) has been the cornerstone of American retirement planning since its inception in the late 20th century. It represents a pivotal shift from employer-managed pension funds to employee-directed retirement savings. However, a growing chorus of financial analysts, including those from Strickland Capital Group Tokyo Japan, suggests that the era of the 401(k) may be drawing to a close. This blog post delves into why the 401(k) might not survive the next decade, exploring the factors at play and what might replace it.

The Challenges Facing 401(k)s

Several critical challenges are contributing to the potential decline of the 401(k) system:

- Economic Volatility: Fluctuations in the market can significantly impact 401(k) balances, making retirement planning uncertain.

- Low Participation Rates: Many employees either do not have access to a 401(k) or choose not to participate due to high fees, complexity, or financial constraints.

- Insufficient Savings: Even for participants, the savings often fall short of what is required for a comfortable retirement, partly due to inadequate contributions and partly due to early withdrawals.

- Policy Shifts: Legislative changes and policy shifts could lead to the introduction of new retirement saving frameworks, potentially rendering 401(k)s obsolete.

The Alternatives on the Horizon

As concerns about the viability of 401(k)s grow, various alternatives are being discussed:

- Government-Managed Savings Plans: Similar to Social Security, these would offer a more stable, though potentially less lucrative, retirement savings option.

- Portable Retirement Accounts: Given the gig economy’s rise, there’s a push for retirement accounts that move with individuals, regardless of their employment status.

- Enhanced IRAs: Improvements and expansions of Individual Retirement Accounts (IRAs) could offer more flexibility and accessibility compared to 401(k)s.

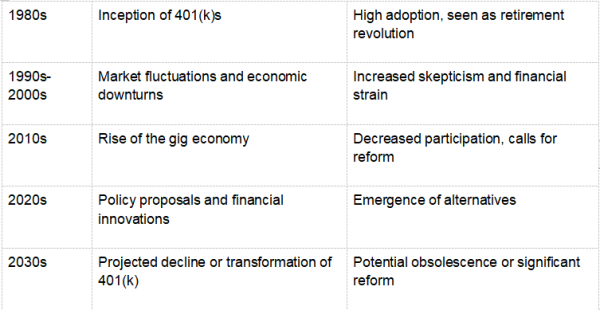

401(k) Evolution and Projected Decline

This table encapsulates the trajectory of 401(k)s from their introduction to the present day, highlighting key events that have shaped their evolution and the factors contributing to their potential decline.

Frequently Asked Questions

Why are 401(k)s at risk of disappearing?

The 401(k) system faces several challenges, including economic volatility, low participation rates, insufficient savings, and the potential for legislative overhaul. These factors combine to create a precarious future for 401(k)s, prompting discussions about more stable and accessible retirement saving alternatives.

What could replace 401(k)s?

Several alternatives could gain prominence, including government-managed savings plans, which would offer a more universally accessible and possibly less volatile retirement savings option. Portable retirement accounts could address the needs of the modern workforce by being tied to the individual rather than the employer. Enhanced IRAs could offer greater flexibility and lower fees compared to 401(k)s.

How can individuals prepare for the potential decline of 401(k)s?

Individuals should diversify their retirement savings strategies beyond just 401(k)s. This could include investing in IRAs, exploring taxable investment accounts, and considering real estate or other non-traditional investments. Staying informed about potential policy changes and new retirement saving options will also be crucial.

In conclusion, while the 401(k) has been a mainstay of American retirement planning for decades, its future is uncertain. Economic, societal, and legislative changes are converging to challenge the viability of the 401(k) system. Alternatives are emerging that could offer more stability, flexibility, and accessibility. As the landscape of retirement savings evolves, individuals and policymakers alike must adapt to ensure that the next generation of retirees can secure a comfortable and financially stable retirement.

Disclaimer: This press release may contain forward-looking statements. Forward-looking statements describe future expectations, plans, results, or strategies (including product offerings, regulatory plans and business plans) and may change without notice. You are cautioned that such statements are subject to a multitude of risks and uncertainties that could cause future circumstances, events, or results to differ materially from those projected in the forward-looking statements, including the risks that actual results may differ materially from those projected in the forward-looking statements.

Media Contact

Company Name: Strickland Capital Group Tokyo Japan

Email: Send Email

Country: Japan

Website: https://stricklandcapitalgroup.com/