After such a brutal year for financial assets, you’d be forgiven for not wanting to go anywhere near the stock market at the moment.

However, for us glass half-full types, we know that with volatility comes great opportunities.

Bear markets are famous for their sharp, counter-trend rallies, which can be just as painful for investors sat on the sidelines, as it can be for bulls when the market declines.

The feeling of FOMO will be all too familiar for many traders who missed the 20% rally in the S&P 500 back in June, for instance.

Now, after a virtually straight 14% decline from the August highs, many are wondering whether another bear market rally is on the cards soon.

Short of having a crystal ball to answer that question, I always find it helps to have a watchlist of potential buy candidates ready, just in case.

In particular, I look for stocks that have seen large corrections, but where that bearish momentum is showing signs of fatigue. This is usually a good setup for a counter-trend rally.

To carry out this search efficiently, I use a stock screener like MetaStock with the following criteria:

- Oversold: RSI Below 40

- Improving Momentum: Price is in a downtrend, but RSI is in an uptrend

Together, these two conditions are known as bullish RSI divergence

3 tech stocks caught my eye from this screen recently: HubSpot, Twilio, and Wayfair – which I will go into more detail below.

Now, this is obviously an unpopular sector at the moment. High duration assets – such as tech stocks that derive most of the earnings from the future – have come under significant pressure from rising interest rates this year.

However, valuation multiples have largely adjusted to this reality, and there is a case to be made for interest rates stabilising soon.

For example, we are starting to see signs of disinflation in commodity prices, inflation benchmarks in China peaking, and supply chain bottlenecks starting to ease. Not to mention the fall in demand from weakening economies.

I’m not saying that inflation will come straight back down to 2%. However, even if it started to fall back towards 6%, or 4%, temporarily, this could give credence to the “FED Pivot” narrative and provide a catalyst for these oversold, under-owned names to rally. A perfect contrarian setup.

Now let’s get into the names I’m looking at…

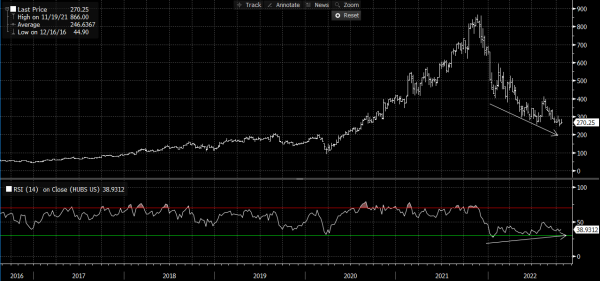

HubSpot

HubSpot is a cloud-based customer relationship management (CRM) platform that has fallen about 72% from its highs.

As you can see in the chart of HubSpot below, the RSI is displaying a classic positive divergence pattern. In other words, the RSI has been making higher lows while the stock price has been making lower lows.

According to technical analysis 101, this suggests that bearish momentum is petering out – paving the way for a bullish reversal at some point.

What’s interesting about HubSpot, is that unlike many other early-stage tech companies (like the other 2 mentioned), it is expected to make a profit this year (EPS $2.28).

The repercussion of this, however, is that it still looks richly valued relative to companies with less earnings visibility. For example, its 2023 EV/Sales multiple is about 6x – the average of its pre-covid range.

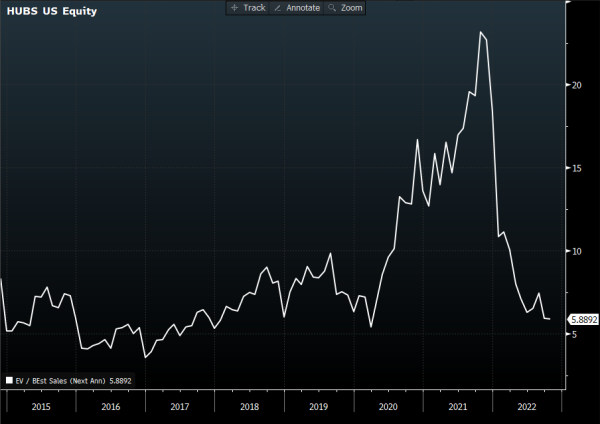

Twilio

Twilio provides cloud-based communication solutions to its customers, and is another stock where the RSI has been rising from low levels all year while the stock price has continued to trend down.

As mentioned, this is usually a sign that a bullish reversal could be coming at some point. Timing it is obviously the tricky part.

Regardless, the risk/reward is starting to look quite attractive now after an 86% drop from its peak.

It’s expected to break-even next year, potentially removing one of the main concerns about these once high-flying tech darlings.

After this year’s correction, it now trades on 2023 EV/Sales ratio of around 2x, which is pretty reasonable given its top-line is expected to grow in the high 20’s for the next few years. As you can see in the chart below, that multiple is at its all-time lows.

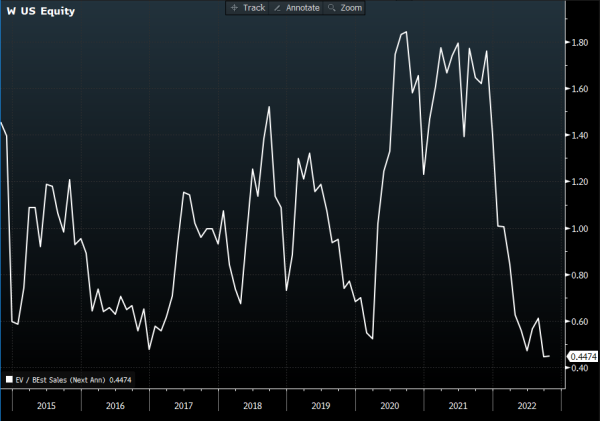

Wayfair

Wayfair is an ecommerce company that sells furniture and household goods.

It has fallen about 92% from its peak and is probably the riskiest of the 3, given that it isn’t expected to break-even until 2026.

This makes it the most sensitive to any further interest rate rises.

Having said that, after such a big correction, its valuation reflects that risk to a degree now. It trades on the cheapest 2023 EV/Sales ratio out of the 3 stocks, at about 0.45x. Again, this is near its own historical lows.

Given its cheaper valuation, Wayfair would have the most upside in terms of multiple expansion if there was a temporary reprieve in interest rates.

As you can see, the chart setup is just what we’re looking for. The RSI is oversold and improving, suggesting that bearish momentum may be coming to an end.

Media Contact

Company Name: The Sovereign Investor

Contact Person: Harry

Email: Send Email

Country: United Kingdom

Website: https://thesovereigninvestor.net/metastock-review/